· 8 min read

Introduction

In 2021, Microsoft co-founder Bill Gates authored How to Avoid a Climate Disaster, a comprehensive plan for reducing global net CO2 emissions to prevent a climate catastrophe. Among the key concepts he discusses is the “green premium,” which refers to the additional cost associated with producing goods or services in a pollution-free or environmentally friendly way. This premium represents the price tag for choosing a greener option.

Early signals of market demand for low-carbon technologies are emerging, bolstered by supportive policies and green subsidies. However, challenges such as untested green premiums persist. The ability of the industry to pass along this premium or to monetise near-zero-emission products as a differentiating attribute depends on the target consumer segment (B2B vs consumer) and geography.

Here is the detailed sector-wise analysis of the green premiums by current estimates:

1. Aviation industry

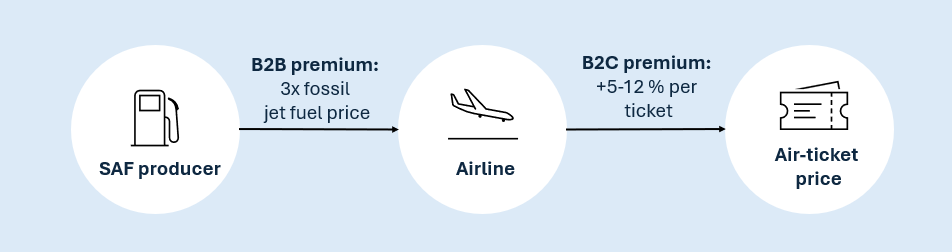

The urgency of Sustainable Aviation: The aviation industry's contribution to global GHG emissions, at around 2% in 2022, has spurred the search for sustainable alternatives. SAF, while promising, faces challenges in adoption due to its limited scale, high costs, and supply chain complexities.

The Green Premium: Sustainable aviation fuels (SAF), as noted, carry higher premiums than traditional jet fuel. The B2B green premium for SAF can be 3x times the current fossil jet fuel price, depending on the fuel's source and the production method. For consumers (B2C), this translates to a 5-12% increase in the price of air tickets.

Figure: B2B and B2C green premium in the Aviation Industry

2. Shipping industry

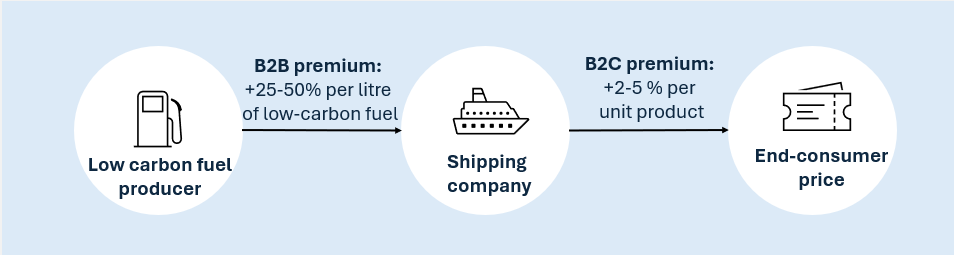

The urgency of Decarbonised Shipping: The shipping industry was responsible for emitting 0.86 Gt CO2e in 2022, accounting for approximately 2% of global greenhouse gas (GHG) emissions. A transition to clean, hydrogen-based zero-emission fuels (ZEF) such as e-methanol and e-ammonia presents a promising pathway to nearly eliminate emissions from this sector. However, adopting these fuels faces significant challenges, particularly in costs and the necessary infrastructure.

The Green Premium: Green shipping technologies such as biofuels and liquefied natural gas (LNG) add a premium of around 25-50% compared to conventional fuel-based shipping operations. Adopting fully sustainable fuels like green ammonia or hydrogen may increase these costs even more. The consumer-facing (B2C) premium varies depending on the shipping company's pricing strategies, but it often ranges from 2-5% per product on the goods transported.

Figure: B2B and B2C green premium in the Shipping Industry

3. Iron and steel industry

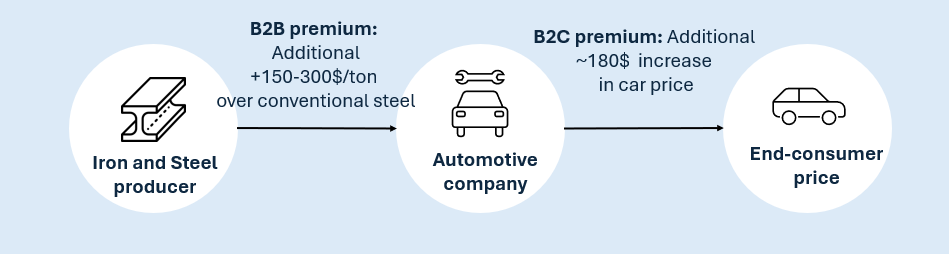

The urgency of Decarbonised Iron and Steel: In 2022, the steel industry was responsible for approximately 3.7 GtCO2e, accounting for 8% of global GHG emissions. Clean hydrogen and carbon capture, utilisation, and storage (CCUS) can decarbonise primary steel. Secondary steel production can achieve decarbonisation through EAF with low-carbon electricity or using scrap materials.

The Green Premium: Green steel production, which involves using technologies like hydrogen-based direct reduction, is expected to see premiums between 150-300 $/ton over conventional steel (differential of green steel and CFR steel prices) in the near term. As hydrogen-based steel becomes more prevalent, some projections estimate that premiums could stabilize as demand grows.

Even with a $200 per ton cost increase due to the adoption of green hydrogen DRI technology over conventional BF-BOF steelmaking, the impact on final products like cars, buildings, ships, and machinery remains minimal. For example, considering that a typical passenger car in the U.S. contains around 900 kg of steel, a $200 per ton increase in steel costs would raise the car’s price by only about $180.

Figure: B2B and B2C green premium in the Iron and Steel Industry

4. Cement industry

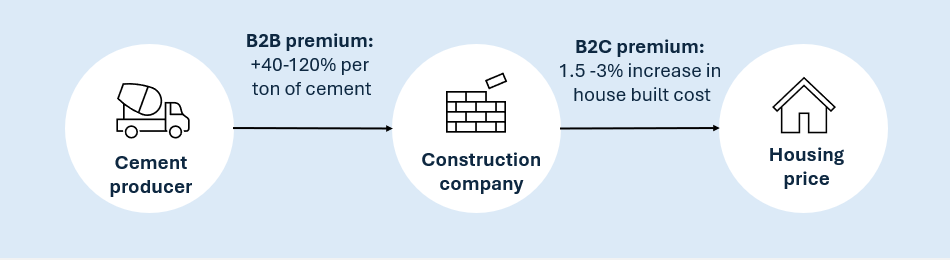

The urgency of Decarbonised Cement: In 2022, the cement industry generated 2.6 GtCO2e, accounting for 6% of global Scope 1 and 2 emissions. The cement industry can use carbon capture, utilisation, and storage (CCUS), clean hydrogen, and clean power to achieve decarbonisation.

The Green Premium: In the cement sector, using low-carbon cement can lead to a B2B green premium of 40-120% per ton of cement, driven by costs from carbon capture and alternative materials. For end consumers, this translates into a B2C green premium of a 1.5-3% increase in the cost of building houses due to the more expensive sustainable materials used. The overall impact on housing prices reflects the increased material costs as sustainable practices are integrated into building processes.

Figure: B2B and B2C green premium in the Cement Industry

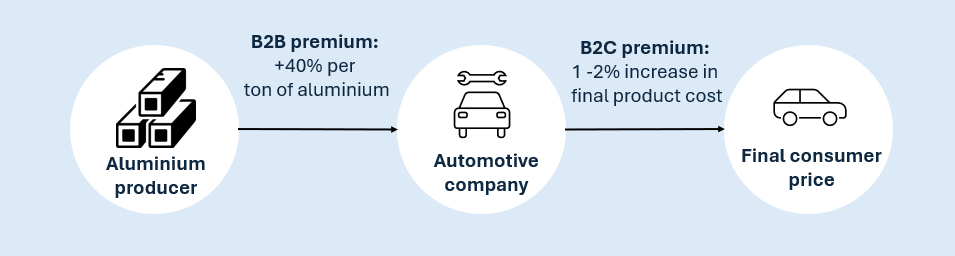

5. Aluminium industry

The urgency of Decarbonised Aluminium: Aluminium is a vital metal for advancing technology and is essential for a net-zero future, playing a key role in electric vehicles (EVs), wind turbines, photovoltaics, and energy storage. In 2022, the aluminium industry was responsible for 1.2 GtCO2e, representing 3% of global Scope 1 and 2 emissions. To reduce emissions, the industry can adopt decarbonisation strategies such as shifting to clean power, increasing the use of scrap materials, and implementing CCUS.

The Green Premium: The cost of producing low-carbon aluminium (B2B premium in $/ton of aluminium) is estimated to be 40% higher than traditional methods, especially when using renewable energy or advanced smelting technologies. In some regions like India and China, where carbon intensity is high, this could rise to nearly 100% due to heavy reliance on coal-based power. For end consumers, such as in the automotive or electronics industries, the B2C premium translates into a relatively modest increase of around 1-2% on the final products

Figure: B2B and B2C green premium in the Aluminium Industry

6. Oil and gas industry

The urgency of the Oil and Gas Industry: In 2022, the Oil and Gas industry was responsible for 5.1 GtCO2e, accounting for 15% of global Scope 1 and 2 emissions. More than half of these emissions originate from methane venting, fugitive emissions, and gas flaring. To address these challenges, five key decarbonisation pathways have emerged: methane abatement, elimination of gas flaring, electrification, carbon capture, utilisation, and storage (CCUS), and the adoption of clean hydrogen.

The Green Premium: Transitioning to low-carbon fuels, including using carbon capture and storage (CCUS) or hydrogen technologies, can add a 20-30% premium over traditional fossil fuels. In some cases, green hydrogen production can drive costs up to 50% higher than grey hydrogen production. For consumers, the increase is less pronounced. Using cleaner fuels may translate into a 3-10% increase in energy bills or gasoline prices, depending on how the additional costs are passed through.

Call to action: How do we bring the premium down?

According to Bill Gates, reducing the green premium depends on many factors. Here are the main three:

1. Innovation: Achieving a low green premium hinges on developing efficient, profitable, and emission-free methods for manufacturing products and delivering services. This encompasses the entire value chain, including production, shipping, marketing, usage, and the end-of-life phase. Research and development and technological advancements are essential in identifying and replacing the processes that contribute to higher green premiums.

One example is Tesla's battery technology. Tesla innovated electric vehicle (EV) batteries and their production, which has driven down the costs of EVs over time. Tesla’s Gigafactory has scaled up battery production, making EVs more affordable and accessible while improving battery efficiency. Such innovations across the value chain—production, shipping, and even end-of-life recycling—are pivotal to reducing the green premium.

2. Financing: Adequate funding drives innovation and transforms production methods to lower green premiums. Financial tools such as green bonds and other sustainable financial products can significantly support these initiatives. Additionally, banks can provide households and businesses with lines of credit and loans to facilitate their transition to more sustainable practices.

Example in Sustainable Finance by European Investment Bank (EIB) (EIB): The EIB has been a global leader in climate financing, offering low-interest loans for renewable energy projects. For instance, the EIB provided substantial financing to offshore wind farms, reducing the cost of these projects and helping make wind power competitive with fossil fuels.

3. Public policy: Government policies are crucial in reducing the green premium. Governments can play a pivotal role by investing in research and sustainable development and incentivising the private sector to follow suit. Policy mechanisms such as carbon pricing, subsidies, grants, green public procurement mandates, tax credits, and codes and standards are some of the impactful tools for encouraging industries to adopt new technologies and reduce emissions.

Example of EU ETS: As of 2023, EU ETS remains the largest compliance carbon market in the world in terms of traded value, and it has driven gradual cross-sector emissions reductions. It reduces the green premium by making carbon-intensive activities more expensive, incentivising industries to adopt cleaner technologies, thus lowering emissions and fostering innovation.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

References

Gates, B. (2021). How to Avoid a Climate Disaster. Available at: https://www.gatesnotes.com/My-new-climate-book-is-finally-here

Hasanbeigi, A., Springer, C., Irish, H., 2024. Green H₂-DRI Steelmaking: 15 Challenges and solutions. Global Efficiency Intelligence. Florida, United States.

Fast Market, S&P Global, RMI